News on the Register of Beneficial Owners

07 Jul 2023Focus on: approval of the forms, the technical specifications and the administrative fees for the communications to the Register of Beneficial Owners

Foreword

The Ministry of Enterprises and Made in Italy (MIMIT) has recently published in the Official Gazette the Decree dated 16 March 2023 on the Approved templates for certificates and counterparts, also in digital formats, on beneficial ownership information and the Decree dated 20 April 2023 on the Applicable administration fees pursuant to art. 8, para. 1, Decree dated 11 March 2022, no. 55.

These measures immediately follow the publication of the Decree of the Ministry of Enterprises and Made in Italy dated 12 April 2023 and it concerns the Approval of the technical specifications of the electronic format of the so-called “Comunicazione unica d’impresa” form.

MIMIT’s decrees arrive about one year after Decree no. 55/2022 of the Ministry of Economy and Finance concerning Provisions on the disclosure of, access, and reference to data and information related to the Beneficial Owners of companies with legal personality, of private legal persons, of trusts producing legal effects being relevant for tax purposes, and of legal entities similar to trusts (hereinafter, also “Regulation on the Register of Beneficial Owners”).

The Regulation implements the provisions under Legislative Decree no. 231/2007 and its following amendments and integrations (hereinafter, also “Anti-money laundering Decree”), which provides for the obligation to register information on the beneficial owners of certain entities in a specified section of the Companies’ Register.

Specifically, the Regulation specifies the content of information to be disclosed, as well as the right to access disclosed data and refers to following provisions for the definition of technical and operating aspects, for the quantification of administration fees, and for the attestation of the system functioning.

Entities concerned by the disclosure obligation

The disclosure obligation concerns three entity categories:

- companies with legal personality which are obligated to register with the Companies’ Register under art. 2188 of the Italian Civil Code (art. 21 of Legislative Decree no. 231/2007), i.e.: limited liability companies, joint stock companies, limited partnerships, and cooperative companies. Simple partnerships are excluded (art. 1 of Ministerial Decree no. 55/2022);

- private legal persons which are obliged to register with the Companies’ Register of private legal persons under Presidential Decree no. 361/2000, (art. 21 of Legislative Decree no. 231/2007), i.e.: associations, foundations, and other private institutions that acquire legal personality by registering with the above register (art. 1 of Ministerial Decree no. 55/2022);

- trusts producing legal effects being relevant for tax purposes, according to the provisions under art. 73 of Presidential Decree no. 917/1986 and trust-like entities established or residing within the territory of the Italian Republic (art. 21 of Legislative Decree no. 231/2007);

The following persons are those responsible for the submission of the communication:

- directors of companies with legal personality (art. 3 of Ministerial Decree no. 55/2022);

- the founder, if alive, or the subjects in charge of the representation and the management of private legal persons (art. 3 of Ministerial Decree no. 55/2022);

- the trustee in trusts or trust-like entities (art. 3 of Ministerial Decree no. 55/2022).

Data concerned by the disclosure obligation

Data and information to be disclosed are those of the beneficial owners of concerned entities (art. 4 of Ministerial Decree no. 55/2022)

For each beneficial owner, the following information must be disclosed:

- identification data

- citizenship

- any exceptional circumstances which may limit access to information on beneficial owners along with a certified e-mail address to exercise the right of objection, as appropriate

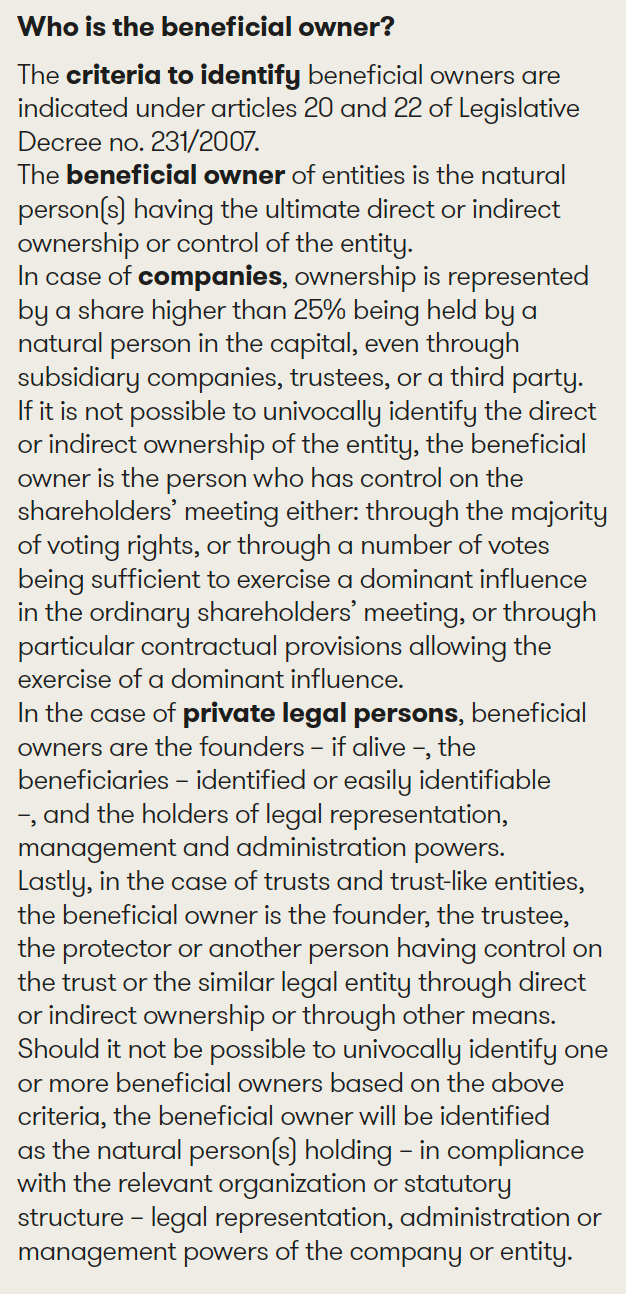

In addition to the above basic information, companies with legal personality should specify the criterion applied to identify the beneficial owner among those specified under art. 20 of the anti-money laundering decree.

On the other hand, private legal persons and trusts (and trust-like entities) must disclose the data indicated under art. 4, para. 1, letters c) and d) of the Regulation on the Register of Beneficial Owners, which are aimed to univocally identify these entities in the proper section of the Companies’ Register, including the register of beneficial owners.

Data and information on beneficial owners must be disclosed in order for them to be registered and kept in a proper separate section of the Companies’ Register, which is, in turn, divided into an autonomous section dedicated to companies with legal personality and private legal persons, and a special section dedicated to trusts and trust-like entities (articles 2 and 3 of Ministerial Decree no. 55/2022).

Procedure and terms to fulfil the disclosure obligation

Data and information on beneficial owners should be disclosed to the competent local Chamber of commerce through a self-declaration pursuant to articles 46 and 47 of TUDA (legal and regulatory provisions on administrative documentation), electronically signed by the person in charge and submitted only electronically, with no stamp duty to apply. The “Comunicazione unica d’impresa” form – whose technical specifications have been recently approved in compliance with art. 3 of Ministerial Decree no. 55/2022 - should be used for all communications.

The first communication must be submitted within 60 days of the entry into force of the decree of the Ministry of Enterprises and Made in Italy, which attests the functioning of the system for the disclosure of data and information on beneficial owners (art. 3 of Ministerial Decree no. 55/2022).

Any following change must be notified within 30 days of the deed amending the previously disclosed data. In case no modifications occur, data must be confirmed within 12 months of the first communication or the last modification or the previous confirmation. Companies with legal personality can confirm data when filing the financial statements (art. 3 of Ministerial Decree no. 55/2022).

Newly incorporated companies and private legal persons must disclose data within 30 days of registration with the Companies’ Register and the Register of private legal persons, respectively, while trusts and trust-like entities must disclose data within 30 days of their foundation (art. 3 of Ministerial Decree no. 55/2022).

Access to the register of beneficial owners

The Authorities and the persons concerned by anti-money laundering obligations (e.g., banks, professionals, etc.) have total access to the register of beneficial owners, in order for them to pursue their institutional objectives and fulfil AML customer due diligence objectives, respectively (articles 5 and 6 of Ministerial Decree no. 55/2022).

On the other hand, access to data by other persons is subject to certain conditions and limitations and is regulated in order to safeguard those beneficial owners who need particular protection (art. 7 of Ministerial Decree no. 55/2022).

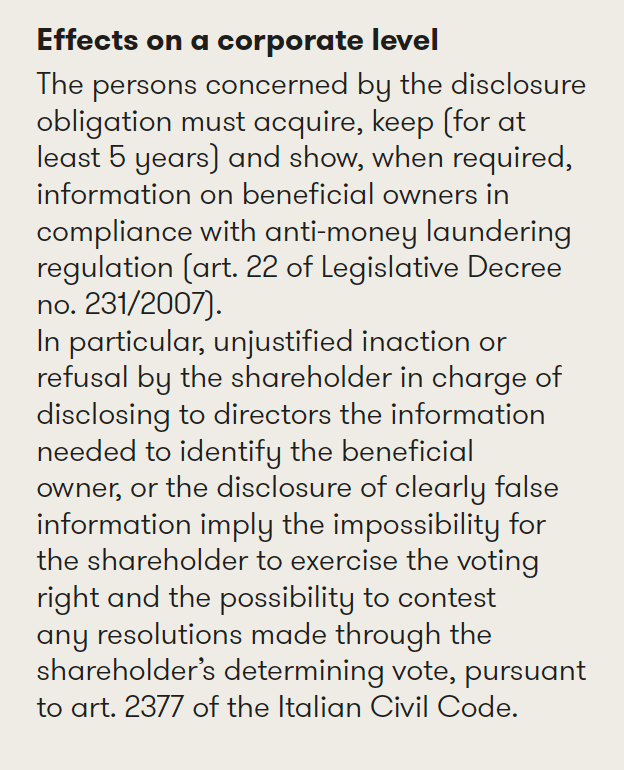

A new and important element is represented by the obligation, for the persons concerned by anti-money laundering obligations (e.g., banks, professionals), to report to the Chamber of Commerce any discrepancy between the beneficial owner declared by the client during the AML customer due diligence and ongoing monitoring and the beneficial owner declared by the client to the Register, which must be consulted when performing the customer due diligence.