Small and medium enterprises: the driver beyond the economy

15 Sep 2021In order to benefit from the supporting measures introduced by the European Union and by the Italian government, companies need to meet not only the “innovation” requirement, as discussed in the previous article, but also the “small and medium enterprise” requirement.

Small and medium enterprises, given their high number, represent the main driver of the economy both in Italy and in Europe. In Italy, companies falling within the European definition of SME are approximately 160 thousand, with a total turnover ranging between 2 and 50 million Euro. With over 94 thousand companies, Northern Italy is the area with the highest number of SMEs (54 thousand in North-West and 40 thousand in North-East), though SMEs are widespread all over Italy (33 thousand in central areas and 32 thousand in Southern Italy).

In the aggregate, the value added produced is equal to 230 billion Euro, of which 39% is produced by SMEs in North-Western Italy, 28% by SMEs in North-Eastern Italy, 18% by SMEs in central Italy, and 15% in Southern Italy (source: Regional Report on SMEs 2021 dated 27 May 2021 – Confindustria/Cerved).

Nowadays, it is not always easy to distinguish a small-medium enterprise from a larger company, since the entrepreneurial environment they operate in is increasingly more evolved, sophisticated and characterized by more or less complex operating, financial and governance relationships, which cannot always be identified easily.

The EU definition of small and medium enterprise is useful to identify those entities that can benefit from public incentives, state aids and de minimis contributions within State subsidies. Therefore, before meeting the requirements related to innovation, innovative SMEs need to meet the requirements needed to be classified as Small and Medium enterprises.

To this regard, the European Commission Recommendation 2003/361/EC dated 6 May 2003 and ministerial decree dated 18 April 2005 aim to:

- provide a practical instrument to help companies identify themselves as SMEs, and

- ensure that EU and Member states’ subsidies are benefitted only by companies that really need them.

As explained below, the characteristics required to be classified as a SME are far beyond the mere dimensional assessment, as it is increasingly more frequent to find very small companies, which, for diverse reasons, can access very significant resources.

The identification of a SME is divided mainly into 4 phases:

- Verify whether the entity classifies as an enterprise;

- Identify the eligibility criteria and their thresholds;

- Interpret the criteria and their correct application;

- Identify the data to be used to ensure that thresholds are met.

1. Verify whether the entity classifies as an enterprise

For this purpose, an entity must carry out an economic activity, regardless of the industry (either goods or services) and of its legal form (partnership, corporation, etc).

2. Identify the eligibility criteria and their thresholds

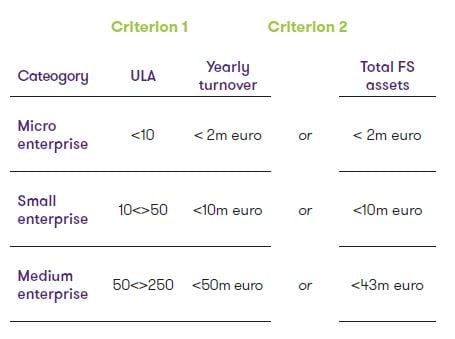

In order to fall within the definition of SME, an enterprise must meet the following two requirements:

- the so-called “ULA” (Unità Lavorative Anno, i.e., the average number of employees in a year) requirement and

- the “turnover” criterion or, alternatively, the “total financial statements assets” requirement.

The choice between the “turnover” and the “total financial statements assets” requirement is provided in order to allow a more homogeneous evaluation of enterprises, depending on their industries (enterprises operating in commerce can have a very different turnover from those operating in the manufacturing industry).

By comparing its own data with the established thresholds, an enterprise can understand whether it falls within the definition of SME or not and, specifically, understand whether it falls within one of the following categories:

- Micro enterprises, with less than 10 “ULA” and a yearly turnover or total financial statements assets lower than 2 million Euro;

- Small enterprises, with “ULA” ranging between 10 and 50 and a yearly turnover or total financial statements assets lower than 10 million Euro

- Medium enterprises, with “ULA” ranging between 50 and 250 and a yearly turnover lower than 50 million Euro, or total financial statements assets lower than 43 million Euro.

3. Interpret the criteria and their correct application

Once the eligibility criteria and their thresholds are identified, data to be used to assess that such thresholds are met must be identified.

ULA – The calculation of the “ULA” of an enterprise takes into account people employed full time, part time, temporarily and seasonally, whether they are either employees, agency-supplied workers, or partners dealing with management activities. On the other hand, the calculation does not include employees under apprenticeship or professional training contracts and employees under maternity or parental leave.

Since “ULA” are expressed in units, those who worked for the enterprise full time for the whole year count as one unit each, while those who worked under temporary, seasonal or part-time contracts are counted as unit fractions, based on the actually worked months.

Yearly Turnover – it is meant as the revenue deriving from the sale of products or services relevant to the last filed financial statements. Such information refers to the item A1 of the income statement, as provided under art. 2425 of the Italian Civil Code.

Total assets – it is meant as the value of an enterprise’s assets. Such information refers to the “Assets” under the balance sheet, as provided under art. 2424 of the Italian Civil Code.

“ULA” and Yearly turnover/Total assets to be considered are those referring to the last approved financial statements. If the company has been newly incorporated and does not have approved financial statements, yet, the above data must be estimated in good faith on the ongoing fiscal year.

4. Identify the data to be used to ensure that thresholds are met

Before calculating the criteria to assess that thresholds are met, it is necessary to assess whether the enterprise is:

- independent;

- associated;

- affiliated.

This check is crucial because, depending on the type of enterprise, the following data are used, respectively, to verify that the threshold is met

- data of the single enterprise;

- data of the single enterprise and part of the data of the associated company(ies);

- data of the single enterprise and all data of the affiliated company(ies).

Definition of independent enterprise

The enterprise (i) must not hold participating interests in other companies, nor must other companies hold participating interests in the enterprise, or, (ii) the participating interest held in one or more companies and/or that held by other or more companies in the enterprise must be lower than 25%.

In this case, the independent enterprise will verify the threshold by considering its own data only (ULA and Yearly turnover/Total assets of the last FY).

The regulation provides for some exceptions as concerns the definition of independent enterprise in those cases in which the participating interest is higher than 25% but is held by specific categories of investors, including:

- universities;

- institutional investors (including regional development funds);

- public holding companies, companies/individuals or groups of individuals regularly investing in risk capital, provided that the total invested amount does not exceed €1,250,000.

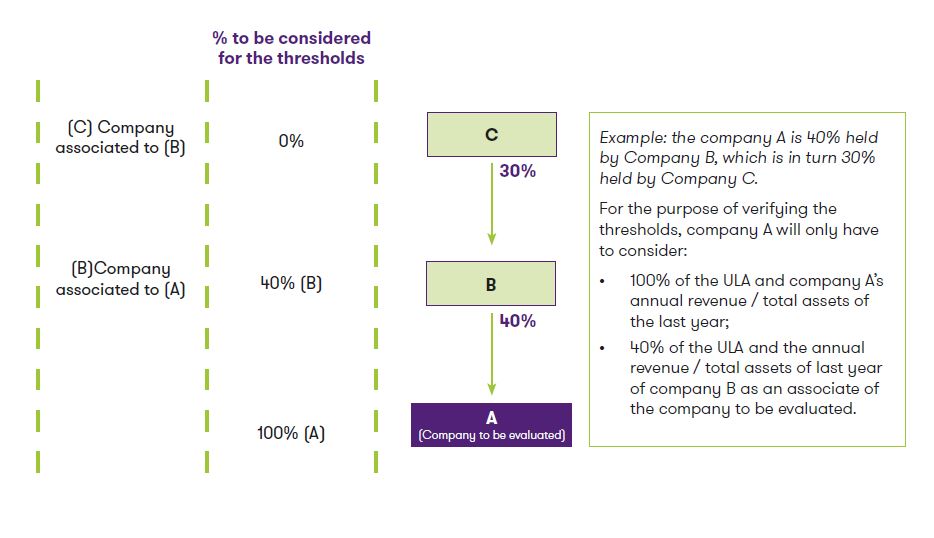

Definition of associated enterprise

The enterprise must hold one or more participating interests in one or more companies and/or one or more companies must hold a participating interest in the enterprise that is higher than 25% and up to 50%. In this case, the enterprise will verify the threshold by taking into account its own data and, pro-quota, the data of the associated enterprise. Data relevant to a company associated to the associated enterprise must not be included in the scope of the evaluation and must not be taken into account for the calculation of the thresholds.

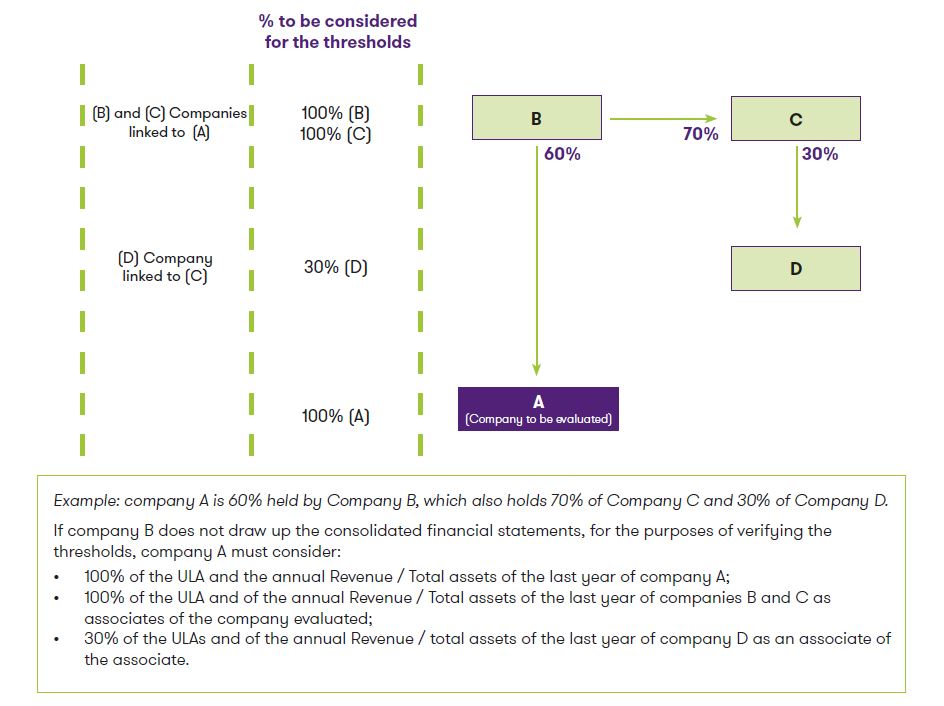

Affiliated enterprise

One or more enterprises are defined as affiliate if one of the following situations occurs:

- an enterprise holds the majority of voting rights into another company;

- an enterprise holds the right to appoint the majority of the governance (BoD, supervisory board, governing board);

- an enterprise, by virtue of a contract or a clause in the articles of association, exercises a predominant power on another company;

- an enterprise, by virtue of an agreement, is able to control the majority of voting rights.

In this case, if the company prepares the consolidated financial statements, the enterprise will verify the thresholds by including consolidated data, otherwise it will consider its own data and 100% of data relevant to affiliated companies.

Considering the turbulence in markets, the current regulation is trying to ensure stability and certainty for those enterprises who are close to exceeding thresholds, providing that a company is no longer a SME only after exceeding such thresholds for two successive years. The same term is provided for the shift from “non-SME" to SME.

Conclusions

Dimension is not the only criterion to consider to classify a company as a SME, as the company’s shareholding independence must also be evaluated. To this regard, the following elements must be considered:

- shareholding structure and participating interests;

- type of shareholders/participating interests (individuals vs public companies vs universities vs risk capital investment companies);

- type of governance;

- predominant influence on one or more companies, directly or indirectly related to the company that is under examination;

- reference end markets, where the company under examination operates.

Given the increasingly more complex and continuously evolving economic environment in which Italian SMEs operate, it is advisable to carry out such verification activity supported by a professional, who can analyse, on a case-by-case basis, the occurrence of the shareholding independence requirement, particularly in the Italian context, where cases in which individuals – often relatives – holding separate companies are frequent.

To this regard, the opinion expressed by the ministerial commission on 13/12/2018 is in favour of considering as affiliates those apparently independent companies whose legal and economic relationships reveal that they constitute – through an individual or a group of individuals acting in cooperation – a unique economic activity, even if the requirements provided for affiliate companies do not occur. Individuals acting in cooperation to exercise an influence on the commercial decisions of concerned enterprises lead to consider the latter as not economically independent from each other.

The realization of this condition depends on the specific circumstances and is not necessarily subordinated to the existence of contractual relationships between these people, nor to their intention to get round the definition of micro, small and medium enterprises. However, point 12 of European Commission recommendation 2003/361/EC dated 6 May 2003 limits this case to those individuals who act in cooperation with separate legal entities in the same reference markets or in similar ones.