Press release

Deliberate market focus drives solid growth

Deliberate market focus drives solid growth for Grant Thornton

by Marco Badiali - Badiali Consulting Co-Managing Partner & Head of Corporate Finance - Staff Location Bernoni Grant Thornton

The recent Law Decree DL 23/2020, turned into Law 40/2020, and better known as Liquidity Decree, introduces some supporting measures to ease the access to bank credit in favour of companies in distress due to the COVID-19 outbreak.

Briefly, it provides for the possibility to access to “collateral” guarantees issued by the State through its entities (Fondo PMI[1] and SACE[2]) whose purpose is granting bank loans to companies affected by the pandemic emergency.

A “deadline” arises from the contents of the regulation, separating “businesses in distress” in two groups, namely:

As far as the first category is concerned, the regulation in point clarifies, also amplifying them, the cases in which the SMEs Fund (Fondo PMI) can intervene. It also provides clarifications on the issuance of guarantees, granting access to entities that were previously excluded, i.e. companies that upon requesting guarantees had exposures highlighted as “inadempienze probabili” (unlikely to pay, UTP) and or “scadute o sconfinanti o deteriorate” (past due).

In short, they shall be UTPs or past due originating from the COVID-19 pandemic emergency. “Doubtful debts” that were Non Performing Exposures (NPE) – as at 29 February 2020 – are excluded, as well as the so-called “distressed” companies - at 31 December 2019 - being classified among distressed businesses as per the EC regulation.

In compliance with COMMISSION REGULATION (EU) No 651/2014 an ‘undertaking in difficulty’ means:

In order to keep ongoing concern situations, although with some operational disruptions determined by the virus outbreak, the Liquidity decree also provides for a kind of “suspension” of the going concern for FYs 2019 and 2020 for those “healthy” companies that, in the lack of Covid-19, would have faced no issues.

The going concern principle is not undermined, but there is an attempt to isolate the COVID-19 phenomenon as an element that might compromise its maintenance. The existence of going concern conditions prior to the COVID-19 outbreak will thus have to be associated to the “foreseeable” existence of post COVID-19 going concern.

Therefore, the simplification introduced concerning the “freezing” of this principle will imply the need to pay higher attention - and with more difficulties if compared with the past - to the business prospective analysis.

It will indeed be necessary not only to highlight and isolate the effects the pandemic emergency has caused and will cause in 2020 on the business performance as well as on the economic and financial balances of the company, but also to have the skills to organise the Company to relaunch after the crisis.

The difficulty to define the reference scenario in which the company will have to compete will be another complex issue. A scenario that surely will be different from the one existing prior to Covid-19.

In our opinion, this exception to the traditional valuation standards is not a guarantee, for the various players involved in the decision-making process needed to grant a loan, of not incurring in other types of problems. Additionally, for the entrepreneur it does not represent an alternative to the rightful decision-making process that has to be developed in order to have access to back credit.

It is evident that risks such as the misuse of credit and the complicity in the misuse of credit, as well as changes in the composition of the company's liabilities further to the access to loans backed up by the SMEs Fund or SACE (credit positions that become preferential) or even material risks of incurring in far more serious offences (e.g. bankruptcy or complicity in this offence) are not superseded by the provision of “freezing” the going concern.

Covid-19 and the state support measures to face the companies’ liquidity crisis the lock-down brought with it, do not modify the reference scenario that should have been already characterised by proper funding strategies.

Our opinion is that the facilitating measures granted (state guarantee on bank financing) and the suspension of the “going concern” assumption (referred to the peculiarities of the intra-Covid period) do not represent a simplification in making decisions on financing. On the contrary, the discontinuity we will record in the market and in the companies’ post-lockdown competitive environment already requires entrepreneurs to have an innovative approach to its own analysis and decision-making process aimed at requesting new finance or at debt restructuring.

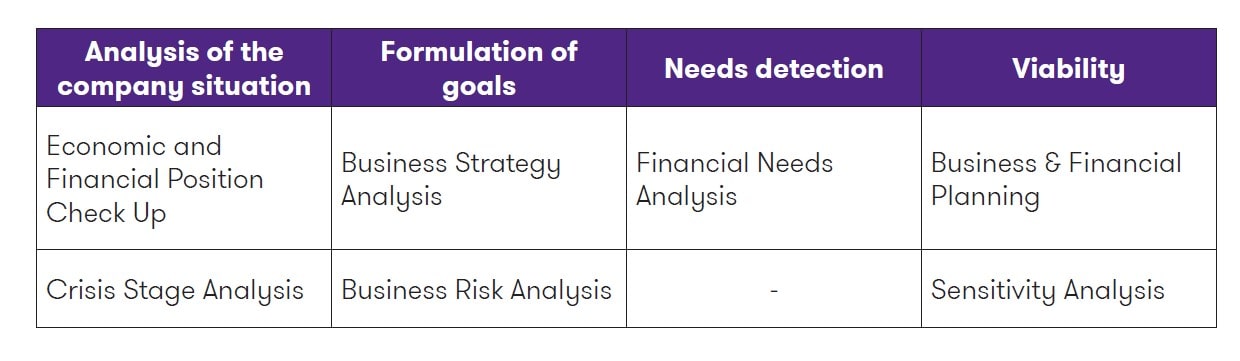

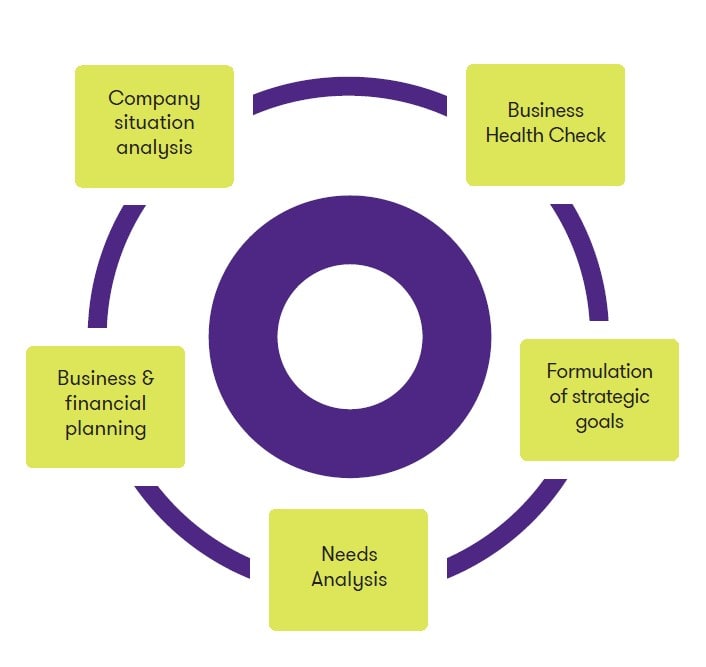

A path that leads to the identification of the correct financing (o re-financing) instrument only at the end of the process that includes analysing the company’s current situation, formulating medium/long-term goals, stating the financial request and verifying its feasibility.

The Debt Advisor’s aim is to support companies along their strategic management path. This path, starting from the analysis of the company’s current situation, enables crisis management with a view to relaunch and, consequently, with a view to feasibility and utility of the financing the bank should grant.

Leaving the idea to redesign a medium-long term vision now, to fully concentrate on short-term needs can lead the company in a state of total passivity, in a condition of strategic dullness that may be lethal, bearing its effects even after the actual emergency period. The proposed model, on the contrary, allows to bond together the concepts of going concern and crisis management on a diverse and primary level: i.e. strategy.

This way, we no longer discuss about “going concern” but about a Business Continuity Management System, nor do we discuss about “crisis management” but about Crisis Management System, precisely in order to highlight the need to develop a holistic approach to entrepreneurial risk as the apex of a pyramid of skills that fits into the decision-making phase. In practice, this is to state the priority of strategy compared to operations and, at the same time, to acknowledge that the bond existing between the two levels of decision and action is not linear, but circular.

The approach to “continuity” and to the “emergency” management becomes part of the strategy, not only preventively but also proactively, influencing how medium/long-term goals - to be preserve in the implementation phase - shall be set.

The unique key to circularly liaise strategy and operational activities in a continuum of decisions and actions is to manage knowledge and its dynamics, the so-called “Knowledge Dynamics Management”. It is clear to many that the worst contingency our Country had to face in this pandemic emergency refers to skills, at all levels, from politics to entrepreneurship, to each single individual who is a member of a bewildered and puzzled community.

This is the new scenario that accompanies the Debt Advisor’s activity, on the assumption to tie in one unique system the often too separated Bank-Advisor-Company trinomial, thus allowing to finally overcome individual behavioural logics, focused on trying to have own personal interests prevail, which are often identifiable in:

This logic has now to be considered as outdated. The role of the Debt Advisor is nowadays even more strategic than in the past, as it is aims first of all to assist the Company with its real financial health-check, to discuss with the management in devising medium/long-term strategies, in finding the best financial instrument to reach the goals set, to assess the economic and financial viability of the request submitted to the Bank.

Through this approach, it will be possible to create mutual trust among the three players of the process and ease the application procedures and decision-making process, consequently determining the issuance of financing that will enable to create an aggregate value that is the sum of the value achieved by each single player involved.

[2] SACE is the Italian State-owned company operating in the financial and insurance sector and specialised in particular in credit insurance.