Business turnaround: industrial vs financial buyers

01 Mar 2023In an M&A operation and, in particular, in case of economic distress of the target, the nature of the buyer, whether industrial or financial, implies a series of considerations, in particular regarding the corporate strategy envisaged for the company, the ability to restore the company thanks to financial rather than operational levers, the ability to recognize a corporate value also in relation to specific tangible or intangible elements.

On the one hand, the main objective of industrial buyers is that of maintaining, or consolidating, their competitive positioning and they aim to exploit the target's know-how to reach industrial synergies and take over new market segments.

On the other hand, financial buyers acquire distressed companies with the aim of realizing the investment in the exit phase, exploiting the value increase created by the implemented recovery plan. In general, industrial players prefer the total purchase of the target, without disclosing the future strategies for the company, while financial players prefer majority acquisitions, but allowing the management to participate in the project.

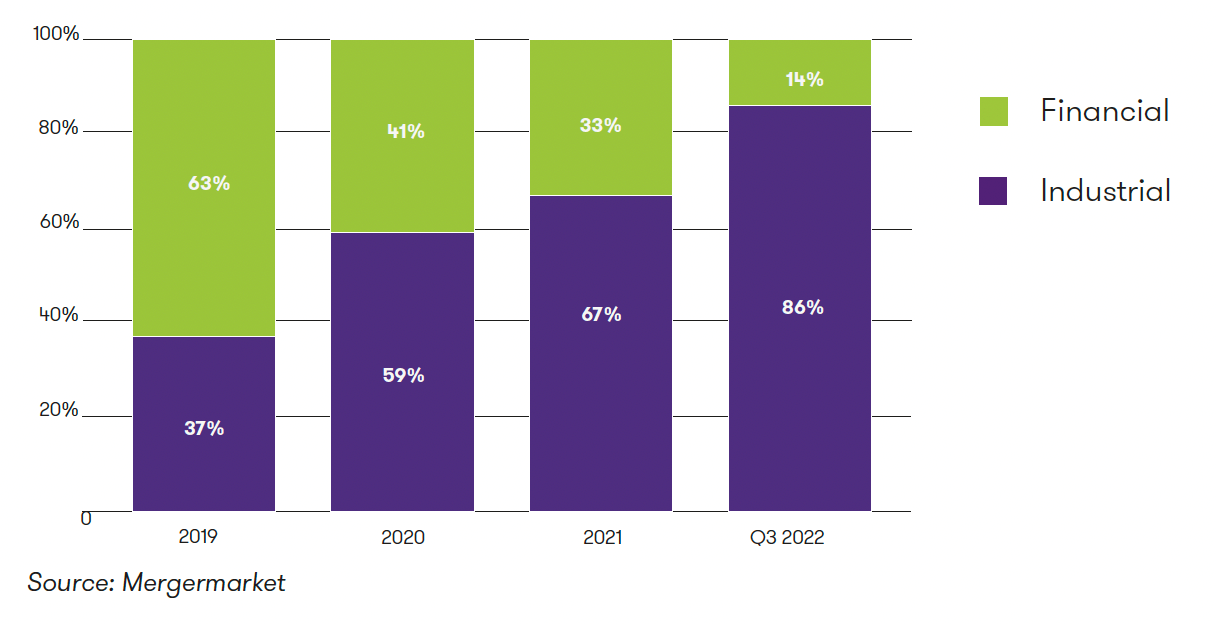

With specific reference to the distressed M&A market, the trend of recent years shows how industrial buyers were predominant: in 2019, 6 deals out of 10 were promoted by strategic buyers, representing more than 60% of the market. On the other hand, the current picture shows a clear turnaround in the market in favour of financial buyers, which represented 67% of the market in 2021 and more than 80% in 2022.

This sudden turnaround is certainly due to the changed economic and financial framework: in fact, strategic buyers are interested in distressed M&A operations in similar industries and, therefore, there are clear limits to the implementation of consolidation or combination projects due to the general uncertainty generated by the pandemic crisis and the changed geopolitical context.

Therefore, the same strategic buyers’ shareholders, which are usually less willing to risk than financial operators, have chosen to wait for a more favourable economic situation to seize opportunities in this sense. Conversely, financial buyers, thanks to the high liquidity available on financial markets and to the opportunities related to the huge sale of so-called non-performing loans promoted by banks, were able to exploit the distressed M&A market more easily. In fact, the same financial players were able to objectively read the risk-return ratio of the distress operation and seize market opportunities.

A growing trend in the number of distressed M&A transactions is expected in the coming months, due, on the one hand, to a further consolidation of financial buyers, thanks to the aforementioned available liquidity, and, on the other hand, to a great restart of those deals promoted by industrial partners, which were previously frozen due to a wait-and-see strategic approach of shareholders.