Press release

Deliberate market focus drives solid growth

Deliberate market focus drives solid growth for Grant Thornton

One of the most important corporate issues originating from the economic downturn caused by the Covid-19 pandemic concerns the recapitalisation of companies, now a necessary step for shareholders in order to face the major losses resulting from the forced stop of consumption and trade in the first six months of this year. In this context, the Corporate Commission of the Milan Board of Notaries issued 3 relevant guidelines on 16 June 2020, aimed at facilitating corporate capitalisation.

Guideline 189 - Clauses establishing a maximum threshold to the right to profit sharing

With the purpose of stimulating and facilitating injections of liquid funds into the most distressed companies, the Corporate Commission of the Milan Board of Notaries deemed as legitimate those shares or shareholdings which entitle the holder to receive a maximum threshold of profits (over the years) which, once reached, can result in the automatic extinction of the equity instrument, regardless of whether it was transfer for a consideration or not.

Therefore, the clauses of companies limited by shares (S.p.A.) including the following provisions are considered legitimate:

It is also specified that, should said clauses give rise, starting from a given moment in the corporate life, to categories of shares or categories of shareholdings or to specific shareholdings which do not entitle to receive profits for the entire residual duration of the company, then their legitimations is subject to the existence of further proprietary rights, such as the right to the distribution of reserves and/or to the distribution of the liquidation surplus.

Guideline 190 - Self-extinguishing shares and shareholdings

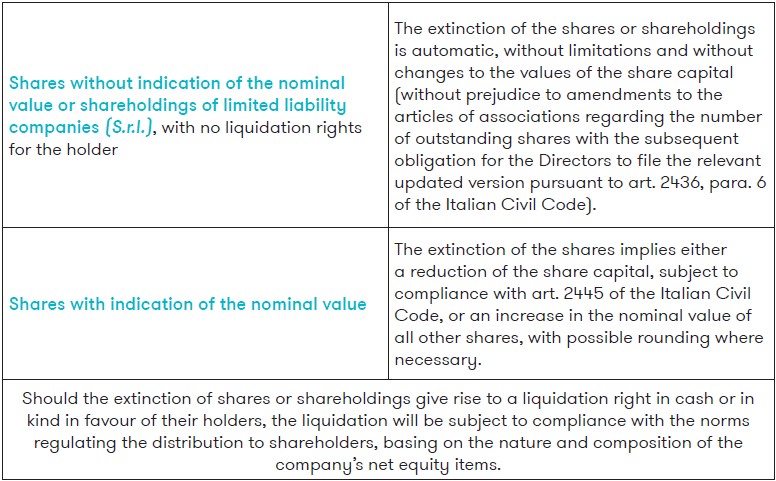

Guideline 190 considers legitimate those clauses of the articles of association of companies limited by shares (S.p.A.) or limited liability companies (S.r.l.) which provide for the automatic extinction of shares and shareholdings at the end of a given period or upon meeting a specific and not merely discretionary condition, such as the attainment of a total amount of profits calculated over time starting from a given moment, even without liquidations rights in favour of the holder of the shares or shareholdings.

In particular:

Guideline 191: Suspension of the norms regulating the compulsory share capital reduction to cover losses during the Covid-19 emergency (articles 2446, 2447, 2482-bis and 2482-ter of the Italian Civil Code; art. 6 of Law Decree 23/2020, so-called Liquidity Decree)

Pursuant to guideline 191, share capital increases for a consideration resolved upon between 9 April 2020 and 31 December 2020, which were not preceded by a share capital reduction to cover losses, are to be considered as legitimate and can be recorded in the Companies’ Register, even when the corporate net equity remains lower than two thirds of the corporate share capital (articles 2446 and 2482-bis of the Italian Civil Code) or lower than the minimum value provided for by law (articles 2447 and 2482-ter) as a result the share capital increase.

Similarly, all other operations with effects on the share capital, which would imply compliance with the provisions above, are to be considered legitimate as well. This interpretation should favour the most distressed joint stock companies - in the contingent Covid-19 emergency - by avoiding to resort to expensive and complex recapitalisations and/or reorganisations.

This position of the Board of Notaries originates from the introduction, under art. 6 of Law Decree 23/2020, of some temporary norms on share capital reduction. In particular, we specify that this new guideline provides for that articles 2446, para. 2 and 3, art. 2447, art. 2482-bis, para. 4, 5 and 6, and art. 2482-ter of the Italian Civil Code (i.e. norms regulating share capital reductions due to losses and share capital reductions below the legal minimum) do not apply to share capital increases operated during FYs closed by 31 December 2020.

Our professionals would be pleased to provide you with any further information you may need.