Press release

Deliberate market focus drives solid growth

Deliberate market focus drives solid growth for Grant Thornton

The so-called “negotiated settlement of the business crisis” is a new crisis settlement instrument introduced with Law Decree no. 118/2021 (turned into Law no. 147/2021), in a particular moment of the global economy, i.e., after the Covid-19 pandemic crisis, with the aim of providing companies with a further possibility to settle business crisis. The regulation on the negotiated settlement of the business crisis is included in Title II of the Business crisis and insolvency code (Legislative decree no. 14/2019, as amended by Legislative Decree no. 83/2022).

The negotiated settlement procedure, in line with the provisions of the European Insolvency Directive, aims to prevent insolvency by promptly identifying and managing crisis situations which could prejudice the going concern, particularly property or economic-financial imbalance situations which make business crisis or insolvency probable, and company reconstruction is reasonably feasible.

The negotiated settlement is an out-of-court procedure conceived for commercial and agricultural entrepreneurs registered with the Companies’ register, who request their competent Chamber of Commerce for the appointment of an expert; such expert plays a crucial role in the negotiation phase and, besides the characteristics required by law to carry out the delicate task, must also have special skills, i.e.: be an able negotiator, a business expert and a crisis law expert.

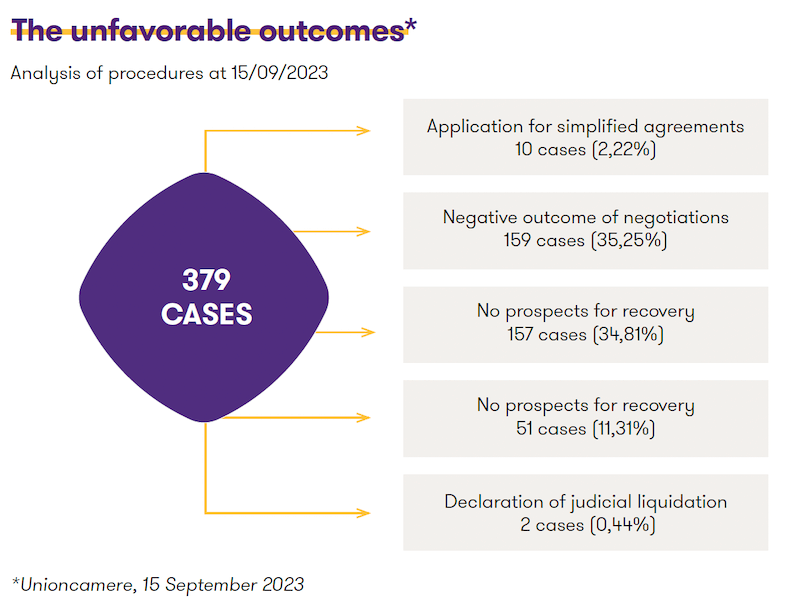

The order of the abovementioned required skills is not random and is consistent with the progress of the procedure. In fact, the negotiation ability is required in the first phase of the procedure, as the expert must be able to negotiate with creditors in a convincing and assertive way, without alerting them too much and trying to understand which of them could approve the company reorganization. At the same time, the business expert figure is crucial, as this must support the entrepreneur in the difficult daily management of the distressed company during the negotiation period. Lastly, the crisis law expert must identify the best outcome of the procedure, which could be any instrument offered by the business crisis and insolvency code, lacking an agreement with one or more creditors. It must be pointed out that some of the possible outcomes (“approved recovery plan”, debt restructuring agreements, and other crisis resolution instruments) are as well solutions aimed at business restructuring and at safeguarding the going concern, leaving as the very last solution only the “simplified liquidating composition” procedure. In support to the above, it must be pointed out that at 15 September 2023 there were 451 dismissed applications, of which 379 had a negative outcome and only 12 ended up with liquidation.

Below is an analysis of procedures at 15/09/2023:

Another peculiarity of the new negotiated settlement procedure is the confidentiality it ensures with reference to the relationships with all stakeholders. However, this fails when wealth protection measures are requested and, therefore, the publicity requirements (publication to the Chamber of Commerce) would disclose the starting of the procedure at issue by the concerned company.

The negotiated settlement of the business crisis, which is a contractual and out-of-court procedure, does not impose the content of the agreements, but only the aim of the same, i.e.: the company reconstruction.

To this end, the evolution proposed by the legislator in this year’s tax reform enabling law is of particular interest. In fact, although the possibility to include the tax settlement procedure within the “negotiated settlement of the business crisis” was mentioned in the drafts of Law Decree no. 13/2023, it was excluded by the provision at the moment of publication of the national recovery and resilience plan (PNRR)-ter. Currently, tax reform enabling law provides for the possibility to introduce within the “negotiated settlement procedure" a composition agreement aimed to write off or delay tax debt. Should this provision be confirmed, it would probably lead to a considerable increase in the number of the negotiated settlement procedure applications.

Reply to request for ruling no. 443/2023 should also be mentioned. In fact, it clarifies that, within the negotiated settlement of the business crisis, taxpayers can propose to the tax authorities a payment deferral of no more than 120 instalments, which should include the whole resulting tax debt, and that instalments can be invariable or increasing, depending on the cash flow resulting from the restructuring plan, whose definition must be confirmed (or modified) by the Revenue Office.