Budget Law 2023, art. 1, para. 100 to 105, introduced tax reliefs for:

- the distribution and transfer to shareholders of intangible and tangible assets recorded in public registries and not used in the corporate activity, as well as for

- the transformation of a business from joint-stock company into a partnership.

The tax reliefs introduced concern in particular i) the possibility to apply a substitute tax (instead of corporate income tax and regional production tax - IRAP) on extraordinary gains on disposals and on reserves subject to taxation on distribution which have been written-off; ii) the possibility to use the cadastral value of buildings, instead of their normal value, to determine said extraordinary gains; iii) a 50% reduction in proportional registration tax rates; and iv) the application of fixed mortgage and cadastral tax.

Below are is an overview of the relevant Budget Law provisions (art. 1).

Para. 100 – subjective and objective requirements

The tax reliefs apply to unlimited partnerships (società in nome collettivo), limited partnerships (società in accomandita semplice), limited liability companies (società a responsabilità limitata), joint-stock companies (società per azioni) and partnerships limited by shares (società in accomandita per azioni) which distribute or transfer the following assets to their shareholders by 30 September 2023:

- intangible assets (lands and buildings), except for capital assets not for business purposes;

- registered tangible assets not used as capital assets in the business activity.

Companies having as their exclusive or main purpose the management of said assets (thus, typically, property management companies) and which will turn into partnerships by 30 September 2023, can also benefit from the tax reliefs above.

The tax reliefs are granted upon condition that:

- the shareholders are registered in the register of shareholders as at 30 September 2023 (in case the register is required); or

- the shareholders are recorded in the register of shareholders (where required) by 31 January 2023 by virtue of a transfer deed with certified date prior to 1 October 2022.

The provision aims at avoiding that persons not previously part of the partnership/corporate structure may enter it just before the distribution or transfer deed to benefit from tax reliefs.

Para. 101 to 104 – substitute tax and other reliefs

The tax reliefs provided under the Budget Law concern:

- the possibility to apply an 8% substitute tax (instead of personal income tax (IRPEF), corporate income tax (IRES) or regional production tax (IRAP) on extraordinary gains on assets distributed/transferred to shareholders or intended for purposes other than the corporate activity, further to a corporate transformation; the substitute tax is equal to 10.5% in case of dormant companies for at least two of the three FYs preceding the one underway when the distribution/termination/transformation was carried out;

- the application of a 13% substitute tax on reserves subject to taxation on distribution written-off further to the transactions above, which can benefit from tax reliefs (tax reliefs which in any case do not apply to transfers of assets, since transfers do not result in the reduction of a net equity reserve, but in a consideration);

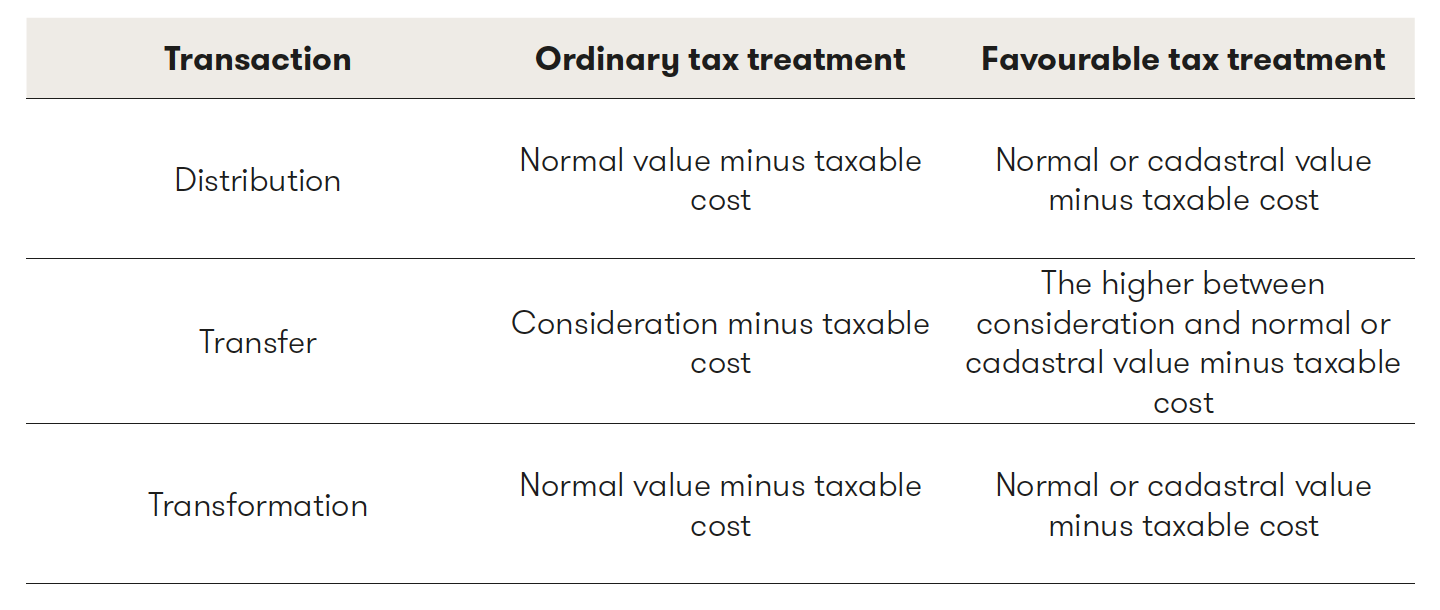

- the possibility to choose whether to refer to the normal vale or to the cadastral value of assets to calculate the extraordinary gain which represents the taxable base of the substitute tax, to be used against the assets’ taxable cost;

- a 50% reduction in registration tax and the possibility to apply fixed mortgage and cadastral tax.

The table below summarises the differences between the ordinary tax treatment and the favourable tax treatment to determine extraordinary gains (taxable base of the substitute tax).

![2_Tax IMAGE.png]()

Para. 103 – Taxable cost of shares or participating interests in case of transformation

The Budget Law specifies that in case of transformation, the taxable cost of shares or participating interests has to be increased by the difference subjected to substitute tax.

By doing so, the higher values of assets in the equity of the transformed company, subjected to an 8% or 10.5% substitute tax, will not be subject to taxation again when the shareholders will transfer their shares/participating interests in the resulting partnership.

Para. 105 – tax payment deadlines

The substitute tax has to be paid as follows:

- 60% of the total amount by 30 September 2023;

- the remaining 40% by 30 November 2023.

Should the matters above be of interest to your company, we invite you to contact your reference partner, or our firm in general, for a more detailed analysis of the possible application of these new provisions.

Our professionals will be glad to provide any further clarification and/or further necessary information.